NIRP Did It: I’m in Awe of How Central-Bank Policies Blind Investors to Risks

by Wolf Richter • Jul 13, 2018 • 0 Comments

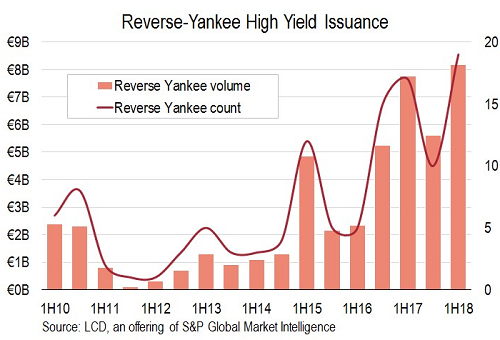

“Reverse-Yankee” Junk Bond Issuance Hits Record.

It’s paradise for US companies looking for cheap money. They range from sparkly investment-grade companies, such as Apple with its pristine balance sheet, to “junk” rated companies, such as Netflix with its cash-burn machine. They have all been doing it: Selling euro-denominated bonds in Europe.

The momentum for these “reverse Yankees” took off when the ECB’s Negative Interest Rate Policy and QE – which includes the purchase of euro bonds issued by European entities of US companies – pushed yields of many government bonds and some corporate bonds into the negative.

By now, yields in the land of NIRP have bounced off the ludicrous lows late last year, as the ECB has been tapering its bond purchases and has started waffling about rate hikes. Investors that bought the bonds at those low yields last year are now sitting on nice losses.

But that hasn’t stopped the momentum of reverse Yankees, especially those with a “junk” credit rating.

Bonds issued in euros in Europe by junk-rated US companies hit an all-time record in the first half of 2018, “taking advantage of decidedly cheaper financing costs in that market,” according to LCD of S&P Global Market Intelligence.

In the first half, US companies sold €8.2 billion of these junk-rated reverse-Yankee bonds, a new record (chart via LCD):

These bonds are hot for European investors who are wheezing under the iron fist of NIRP that dishes out guaranteed losses even before inflation on less risky bonds. Anything looks better than bonds with negative yields.

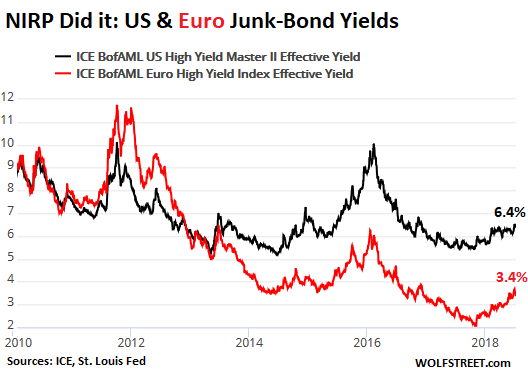

And here is why it makes sense for US companies to chase this money: It’s still ultra-cheap particularly for lower-rated companies. The chart below shows just how much sense it makes for the companies – though investors are going to have their day of reckoning.

The euro high-yield ICE Band of America Merrill Lynch index currently shows an average effective yield of 3.4% (red line). These are junk-rated companies!

The equivalent index for the US shows an effective average yield of 6.4% (black line). This is a spread between the two of 3 percentage points – thanks to a different central-bank regime.

Also note how during the euro debt crisis in 2011 and 2012, junk-bond yields spiked in both markets, but a lot more in the Eurozone to where the average euro-denominated bonds yielded well into the double digits:

As the chart shows, the average euro junk-bond yield, while still ludicrously low at 3.4%, has surged from even more ludicrously low levels last year, when it fell below the 10-year US Treasury yield, a hilarious distortion that I pooh-poohed a few times not without some relish. In October 2017, the average euro junk-bond yield fell as low as 2.08%.

At the time, investors took sizeable credit risks on those bonds and are getting paid less than the rate of inflation to take those risks. Those investors are now getting punished. When yields rise, bond prices fall by definition. Investors can either sell those bonds at a loss or hold them to maturity at a yield of just over 2%, if a default doesn’t x out that option.

In terms of reverse Yankees, they’re ultra-cheap money for US companies. For investors, they’re engaging in similar credit risks with those euro-bonds as they do with dollar-bonds issued by the same US companies, but they’re getting paid only about half as much to take those risks!

I’m just in awe of how central-bank policies have blinded investors to risks and have altered rational thinking.

And yet, the US high-yield market – both for bonds and leveraged loans – is still richly valued as well, and yields are still very low. Credit is flowing easily and in large quantities despite the Fed’s ongoing efforts to tighten financial conditions – or “remove accommodation,” as it likes to say. And this ebullient junk-bond market in the US will see higher yields and lower prices. So the chart above is comparing one ebullient market (black line) with a vastly more ebullient market (red line) – though both markets have already taken a licking and are facing bigger lickings.

Rising interest rates have a peculiar effect. Read… Leveraged-Loan Risks Are Piling Up

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.